Best AI Personal Finance Tools (2026)

Most personal finance apps still treat you like a spreadsheet that forgot to fill itself in. You link your accounts, the app dumps a wall of transactions on you, and then it's your job to drag everything into the right bucket every Sunday night. The "AI" was a marketing sticker.

That changed over the last two years. The good apps now read your spending the way an attentive accountant would: they tag transactions correctly without a month of training, answer plain-English questions, and a few will actually move cash, cancel subscriptions, or negotiate a bill for you. The gap between the apps that do this well and the ones that slapped a chatbot on an old codebase is wide.

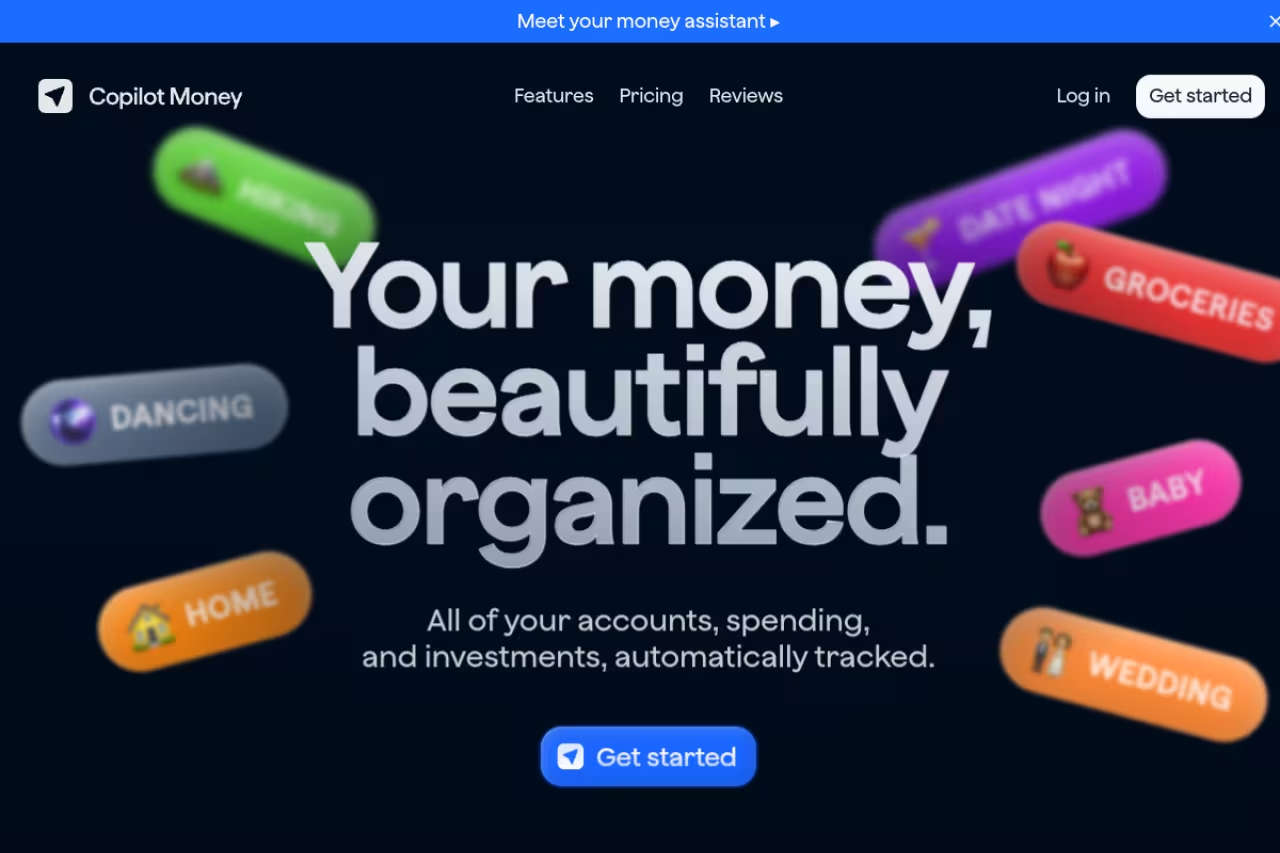

My top pick for most people is Copilot Money. The auto-categorization is the most accurate I've used, the design stays out of your way, and it covers spending, investments, and net worth in one place. The catch is it's iOS and Mac only, so Android users should jump to Monarch or Cleo below. This guide is for anyone who wants their money tracked without becoming a part-time bookkeeper: founders, operators, and people who just want a clear answer to "can I afford this."

Quick comparison

| Tool | Best for | Price | Standout |

|---|---|---|---|

| Copilot Money | Apple users who want the best AI tagging | $95/yr | Categorization that actually learns |

| Monarch Money | Couples and cross-platform households | $99.99/yr | Shared budgets + flexible planning |

| Cleo | People who avoid their finances | Free; Plus $5.99/mo | A chatbot that roasts your spending |

| Rocket Money | Killing subscriptions and lowering bills | Free; Premium ~$6-12/mo | Bill negotiation done for you |

| Origin | Spending plus wealth planning | $1 first year, then paid | AI advisor across investments + goals |

| YNAB | Hardcore zero-based budgeting | $109/yr | Discipline that changes behavior |

| Help | Free net worth and portfolio tracking | Free | Investment dashboard at no cost |

| ChatGPT / Claude | Custom analysis on your own data | $20/mo each | Ask anything, no account linking |

Copilot Money: the best AI tagging on Apple

Copilot Money is the app I recommend first to anyone on an iPhone or Mac. It pulls in your bank accounts, credit cards, and investments, then categorizes every transaction automatically. The difference from older apps is that the model learns your patterns fast. Recategorize a merchant once and it sticks, instead of fighting you every billing cycle. It's best for Apple users who want a clean tracker that handles spending, investing, and net worth without manual tagging.

Pricing is $95 per year (about $7.92 a month) or a monthly option, and you can test the whole app before linking a single account, per Copilot's site. No ads, no data selling.

The standout is the categorization engine plus investment tracking. It reads transactions, flags unusual spend, tracks portfolio allocation across brokerage and retirement accounts, and lets you log real estate by address for net worth. It feels like one tool instead of three bolted together.

The catch: there's no Android app. If half your household is on a Pixel, this is a non-starter, and you should look at Monarch instead.

Monarch Money: the best for couples and mixed devices

Monarch Money became the default household recommendation after Mint shut down, and it earned the spot. It runs on iOS, Android, and the web, so two people on different phones can share the same budget, goals, and net worth view. The AI handles categorization and surfaces trends, while the planning tools stay flexible instead of forcing one rigid method on you. It's the pick for couples and anyone splitting finances across different devices.

Monarch runs $99.99 per year (roughly $8.33 a month) or $14.99 monthly, with a Plus tier at $199 a year for business owners and serious planners, per multiple 2026 pricing reviews. Your first week is free, and a welcome code often knocks 30% off year one.

The standout is collaboration plus connectivity. Both partners get real-time access, you can assign transactions to people, and the bank connections are among the most reliable in the category.

Where it falls short: it's pricey, and the AI advice is more "smart summaries" than a true advisor that tells you what to do next. If you want a bot with opinions, keep reading.

Cleo: the AI that roasts you into saving

Cleo is the odd one out, and that's the point. Instead of dashboards, it's a chat-first AI you talk to like a blunt friend. Its famous "Roast Mode" reviews your purchases and mocks your $14 lunch deliveries until the shame does what willpower couldn't. There's a "Hype Mode" too, if encouragement works better for you than insults. It's built for people who open finance apps, feel anxious, and close them.

The core money tools (tracking, budgeting, and the chatbot) are free. Cleo Plus is $5.99 a month and unlocks cash advances up to $250 plus credit features, per Cleo's 2026 lineup. Pro at $8.99 adds 2.75% APY savings and voice chat; Builder at $14.99 raises advances to $500.

The standout is engagement. For someone who has never stuck with a tracker, a chatbot that texts back beats a perfect spreadsheet they'll never open.

The catch: cash advances carry express fees of roughly $3.99 to $9.99 each on top of the subscription, and the analysis is shallower than Copilot or Monarch. It's a behavior tool, not a wealth dashboard.

If you're building a workflow where AI handles the boring parts of your day, finance included, Dupple X bundles the major AI assistants in one subscription so you can test these approaches without paying for five tools at once.

Rocket Money: the subscription assassin

Rocket Money does one thing better than anyone: finding money you're quietly leaking. Its algorithm scans linked accounts, surfaces every recurring charge (including the free trials that turned into $12 monthly habits), and cancels them for you. No phone calls, no chasing customer service. It's for anyone who suspects they're paying for subscriptions they forgot about, which is most of us.

The free tier covers subscription detection and spend tracking. Premium runs on a pay-what-you-want model between roughly $6 and $12 a month with a 7-day trial, per Rocket Money's pricing, and unlocks cancellation plus net worth tracking.

The standout is bill negotiation. Submit a bill and Rocket Money's team tries to lower it, claiming around an 85% success rate. You only pay if they win, but the fee is a steep 35% to 60% of the first year's savings, per CNBC's review of negotiation services. Where it falls short: it's a leak-stopper, not a full financial brain, and the budgeting is basic next to Monarch or YNAB. Use it alongside a primary tracker.

Origin: spending meets real wealth planning

Origin refuses to treat budgeting as a separate room from the rest of your finances. Its AI advisor, Origin AI, answers questions grounded in your actual data, so you can ask whether this month's spending is hurting your retirement and get a real answer instead of a generic tip. It pulls spending, investments, net worth projections, and even tax and estate tools into one view, for people whose finances have gotten too complicated to split across separate apps.

Origin runs frequent promos, currently $1 for the first year before standard paid pricing, per Origin's site. It's on iOS, Android, and Mac.

The standout is the connected advisor. Because Origin AI sees your portfolio, goals, and cash flow at once, its answers weigh trade-offs a budget-only app can't.

The catch: a do-everything app can feel less polished at any single job than a specialist. If you only want spending tracked, it's more than you need. For more money assistants, my best AI for finance guide goes deeper.

YNAB: the budget that changes behavior

YNAB (You Need A Budget) is the least flashy app here and the most effective for one goal: getting you to stop living paycheck to paycheck. It uses zero-based budgeting, where every dollar gets a job before you spend it. There's no headline AI feature, and that's fine. What YNAB sells is a method that genuinely rewires habits, for people who want to fix their relationship with money and will do the work it requires.

It's $109 per year ($9.08 a month) or $14.99 monthly, with a 34-day free trial and no card required, per YNAB's pricing. Students get a free year.

The standout is behavior change. YNAB users routinely report saving real money in their first few months because the method forces intentional decisions.

Where it falls short: the learning curve is real and the manual approach is more work than passive trackers. If you want hands-off, this isn't it.

Help: the best free net worth tracker

Help (formerly Personal Capital) remains the strongest free option for watching wealth, not just spending. Its dashboard tracks net worth, cash flow, and investment portfolios in one place, with a retirement planner and a fee analyzer that flags expensive funds eating your returns. It's for people with both bank and brokerage accounts who want one free dashboard.

The Personal Dashboard is genuinely free. Help makes money from optional managed investing (0.49% to 0.89% of your portfolio annually), so expect occasional advisor outreach. The standout is the investment view at zero cost; few free tools show portfolio allocation, hidden fees, and retirement projections this clearly.

The catch: the interface feels dated next to Copilot and Monarch, and the advisor calls can be persistent. Use it as a wealth tracker, not a daily spending app.

ChatGPT or Claude: roll your own analysis

Sometimes the best AI finance tool isn't a finance app. Export transactions to a CSV, and ChatGPT or Claude will analyze your spending, build a budget, model a debt payoff plan, or answer "where did $2,000 go last month" in seconds, with no account linking and no monthly app fee. It suits privacy-conscious people and anyone who wants custom analysis a rigid app won't do. Both run about $20 a month, and the free tiers handle light work; see my best AI assistant comparison if you're choosing between them.

The catch: you do the plumbing. There's no auto-sync, no live balances, and you should never paste full account numbers. It's a strong supplement, not a replacement for a connected tracker.

How to choose

Start with your platform and your problem, not the feature list.

On Apple and want the cleanest tracker? Pick Copilot Money. Household spanning iPhone and Android? Monarch is the safer call. Avoid finance apps entirely? Cleo's chat format is the only one likely to stick. Want behavior change over passive tracking? YNAB is the proven choice. Mixing serious investing with day-to-day budgeting? Origin or Help pulls both into one view. And run Rocket Money alongside whatever you pick if wasted spend is your real problem.

One rule worth following: don't pay for two overlapping apps. Pick one primary tracker, add at most one specialist (usually Rocket Money for subscriptions), and stop there. The same logic applies to AI subscriptions generally, which is the idea behind Dupple X.

Want help wiring AI into more of your week than just your budget? Dupple X gives you the top assistants in a single subscription, and the top tools directory tracks what's worth paying for as this category keeps moving.

FAQ

What is the best AI personal finance tool in 2026?

For most people on Apple devices, Copilot Money is the best all-around pick: its AI categorization is the most accurate and it covers spending, investing, and net worth in one app. Cross-platform households are better served by Monarch Money, and people who avoid budgeting tend to stick with Cleo's chat-based approach.

Are AI budgeting apps safe to link to my bank account?

Reputable apps use bank-grade encryption and read-only connections through aggregators like Plaid, meaning they can see transactions but cannot move your money. Copilot, Monarch, Rocket Money, and Help all use this model. The real risk is reusing weak passwords, so enable two-factor authentication and never paste full account details into general chatbots.

Is there a free AI personal finance app worth using?

Yes. Help offers a fully free net worth and investment dashboard, Cleo's core tracking and chatbot are free, and Rocket Money's free tier finds your subscriptions. You only need to pay when you want advanced budgeting, bill cancellation, or deeper investment tools.

Can ChatGPT actually help with personal finance?

It can, for analysis and planning. Export your transactions to a CSV, upload it to ChatGPT or Claude, and ask it to categorize spending, build a budget, or model a payoff plan. It won't sync to your accounts or show live balances, so treat it as a smart analyst that complements a connected tracker. My ChatGPT for stock trading guide covers the investing side.

Does Rocket Money really cancel subscriptions and lower bills?

Yes, those are its core features. The free tier surfaces recurring charges, and Premium handles cancellations for you. Bill negotiation is run by Rocket Money's team with a claimed success rate near 85%, but it charges 35% to 60% of the first year's savings when it wins, so it only makes sense on large, negotiable bills like internet or insurance.

How much should I expect to pay for an AI finance app?

The category has settled into a roughly $7 to $15 a month range. Cleo Plus starts at $5.99, Copilot is about $7.92 a month billed annually, Monarch runs $8.33, and YNAB lands at $9.08. Free options exist (Help, plus the free tiers of Cleo and Rocket Money), so try those before committing to a paid plan.